Property Market Review June 2019

SUBDUED Q1 FOR SCOTTISH COMMERCIAL PROPERTYDuring the first three months of the year, commercial property sales in Scotland totalled £763m, this is a decrease of 21% (£203m), when compared to Q1 2018. The research from the Scottish Property Federation (SPF), has identified that the fall can primarily be attributed to fewer high value transactions, with £5m plus sales down almost a third. The commercial property investment data emphasises an increase in investor appetite for alternative property asset classes, including hotels. Highlighting the continuing popularity of the Scottish capital, which currently accounts for 35% of the market by value, Director of the SPF, David Melhuish, commented: “For investors, Edinburgh remains a hotspot, while more broadly, low growth and lack of certainty in the economy is weighing down on activity“. Over the last four years, commercial property sales across Scotland totalled £3.03bn, the lowest rolling annual total since Q2 2014.

COMMERCIAL PROPERTY INVESTMENT VOLUMES UNDER PRESSUREThe recently released ‘Market in Minutes: UK Commercial’ publication from Savills has outlined that the uncertainty surrounding Brexit has continued to negatively impact investment volumes this year – the sector has experienced an abnormally slow start to 2019. Commercial property investment reached £15bn by the end of May. To avoid the first half of 2019 being the slowest half since 2013, a further £5bn would need to be transacted in June. With political uncertainty weighing, it’s looking unlikely that investment volumes will hit £63bn – the five-year average. The review highlighted one particular new driver of demand this year; there has been a surge in investment by occupiers buying in freeholds, which represents 14% of the market. Although distorted by the £1.1bn purchase of 25 Canada Square by Citigroup, it seems the changes brought into lease accounting by IFRS 16 will start to see occupiers alter their leasehold/freehold strategy.

SOUTH EAST OFFICES BUCKING THE TRENDAccording to commercial property consultancy, Lambert Smith Hampton (LSH), the office market in the South East is opposing the overall trend of ongoing uncertainty, with take-up 3% above the annual average. Following two years of under par activity, takeup in the South East rebounded, with Basingstoke, Reading and Slough, top performing areas. Kevin Wood of LSH commented: “There is a growing sense that the South East is moving into an exciting new phase of growth and change, backed by major transport infrastructure improvements. Take-up of prime space is a striking feature of the market, underlining the importance of quality provision to stimulate demand. More than ever, occupiers are focusing on their space as a magnet to attract and retain staff and add real value to their business.” In 2018, Grade A take-up reached a 17 year high of 3m sq. ft, as strong inward investment drove exceptional levels of performance across the region. Rapid growth of flexible office providers reflects a shift in occupier demand and a race for market share, with the TMT (Technology, Media and Telecommunications) sector at the forefront of occupier demand in the South East. |

| Back to top |

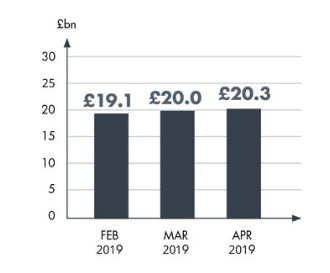

HOUSE PRICES HEADLINE STATISTICS |

|||||||||

|

| Back to top |

HOUSE PRICES PRICE CHANGE BY REGION |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| Back to top |

AVERAGE MONTHLY PRICE BY PROPERTY TYPE – APR 2019 |

|||||||||||

Source: The Land RegistryRelease date: 29/09/2019

|

| Back to top |

MORTGAGE ACTIVITY |

|

| Back to top |

| It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. |